Download the House View PDF here.

1. Market Review

By Can-Luca Köymen, Portfolio Manager

Crushing inflation

The month of September slowly marked the end of summer, but not the end of inflation. Once again, the market drivers were mainly the inflation figures and decisions made by central banks. US CPI numbers came in significantly higher than the consensus expected, and equity market indices tumbled, resulting in their worst day of 2022. Naturally, the FED followed up with an additional 75 bps rate hike and signaled that further larger rate hikes were to be expected. Overall, this resulted in weak markets, with the NASDAQ down 10.5% over the month. Compared to previous months, however, crypto assets showed signs of a decoupling.

Crypto assets – decoupling and bottoming coinciding?

Throughout the first half of the month, weak equity markets posed a challenging environment for crypto. Disappointingly, the successful Ethereum merge did not result in a bullish market dynamic, and we observed short-lived market weakness post merge. Ever since then, though, there have been signs of a decorrelation correspondingly decoupling crypto from traditional markets.

In a market storm, where FX rates exhibited excessive volatility, government bonds suffered meltdown driven by a rate hike, and tech continued to tumble. Crypto markets in contrast showed relative resilience. In fact, over the last two weeks BTC outperformed the NASDAQ by more than 8.25%. This tentative decoupling has coincided with historically attractive fundamental valuation levels.

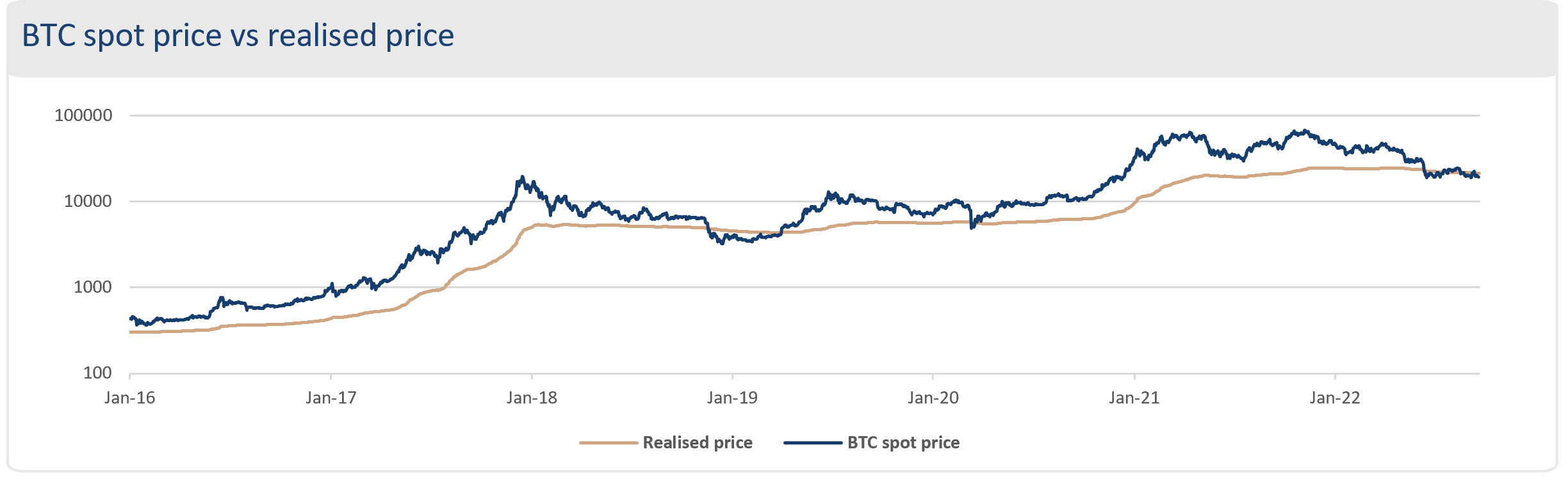

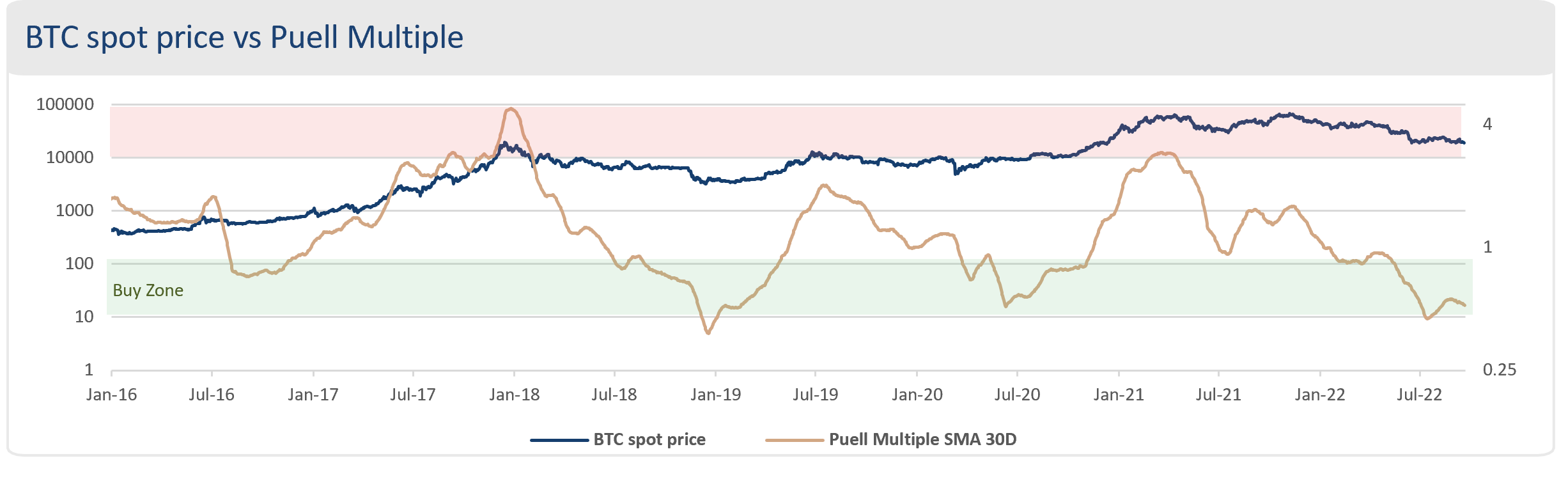

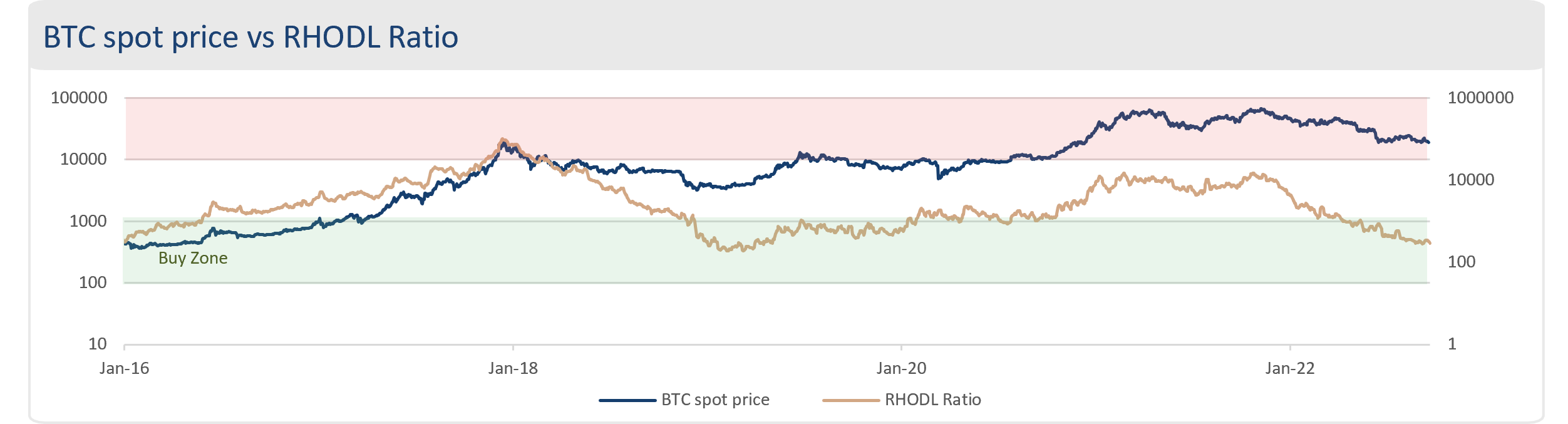

Numerous on-chain data insights point to a potential bottoming in crypto. Bitcoin has been trading below its “realised price” for most of the month. Other key ratios confirm these signs of a potential bottoming. The “Puell Multiple” and also the “RHODL ratio” are hovering around ranges indicating a fundamental undervaluation of bitcoin (please see next page for an explanation of these ratios).

The constellation of these three important ratios supporting the undervaluation is rare and usually coincides with market bottoms not only for bitcoin but also for crypto assets in general.

These periods have historically offered attractive windows in which to consider accumulating bitcoin, such as during the Crypto Winter of 2018/2019.

NASDAQ and others have entered the fray

The second largest stock exchange in the world has announced a major push into crypto. Initially, NASDAQ plans to offer custody solutions for BTC and ETH. With custody as a key foundation, NASDAQ will then explore the development of other services such as trading. NASDAQ venturing into crypto is a major milestone that could make crypto conveniently accessible to many new potential investors.

Other household names have also moved to establish a strategic foothold in crypto, with Nomura setting up a digital asset business in Switzerland. Also, Wall Street giants Fidelity, Citadel, and Charles Schwab have confirmed a collaboration to launch a cryptocurrency exchange.

Spring follows winter

The Ethereum merge was successful and went smoothly. Yet, as an Ethereum co-founder said after the merge, there is still a long way to go with further updates to follow. In the medium-to-long term, we see the merge as a key factor in helping the crypto asset class continue to mature, and the recent tentative evidence of a decoupling are signs that this maturing has already begun.

September marks the beginning of autumn, whereas crypto markets are already in winter. However, a winter where NASDAQ and other big-name traditional finance players enter the crypto space seems not that frosty at all. And, as we know, winter is always followed by the most beautiful season of the year. Still, before spring can blossom, the currently raging macro storm must first calm down, which can only happen once inflation is somewhat under control.

Realised price

Realised price is a metric that uses on-chain data to estimate the cost basis of current BTC holders by calculating an alternative total market cap that considers the price at which each bitcoin was last moved. A spot price below realised price signals an undervaluation and has historically offered attractive accumulation periods.

Puell Multiple

The Puell Multiple examines the fundamentals of mining profitability and how they shape market cycles. It is calculated by taking a ratio of daily coin issuance (in USD) and its 365D moving average. Lower values indicate that miner profitability is relatively low and that miners may consider reducing hash power, which indirectly reduces selling pressure on liquid supply. A low reading typically points towards a good buying opportunity.

RHODL Ratio

The RHODL Ratio evaluates the movement of coins on a short time frame versus a longer time frame. To be more precise, it compares “unspent coin balances” that are only two weeks old with older coins that have not been moved for one to two years. By considering the realised price of these younger and older coin balances, the ratio can give insights into how large the imbalance between longer term holders and relatively new investors is in terms of profitability. An extremely large reading points to an overheated market and, vice versa, low readings signal an oversold market.

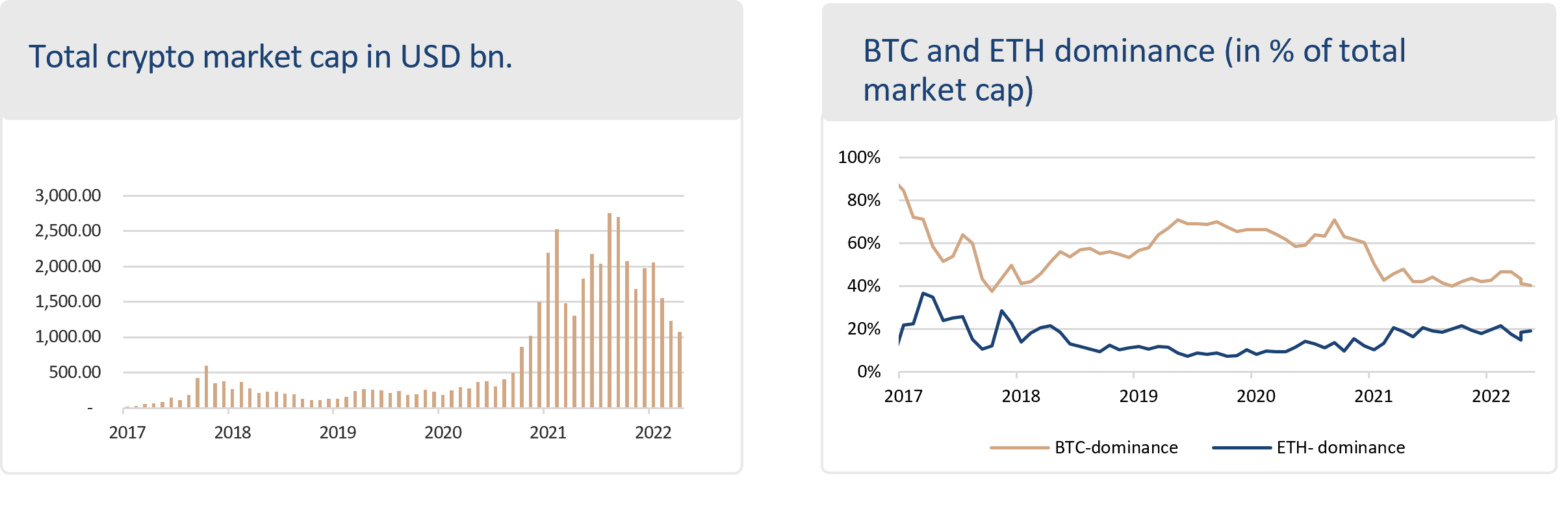

Crypto market capitalisation & dominance

The total crypto market cap has lost –4.5% in the month of September. Ethereum has lost –2.0% in dominance, mostly after the merge sell-off.

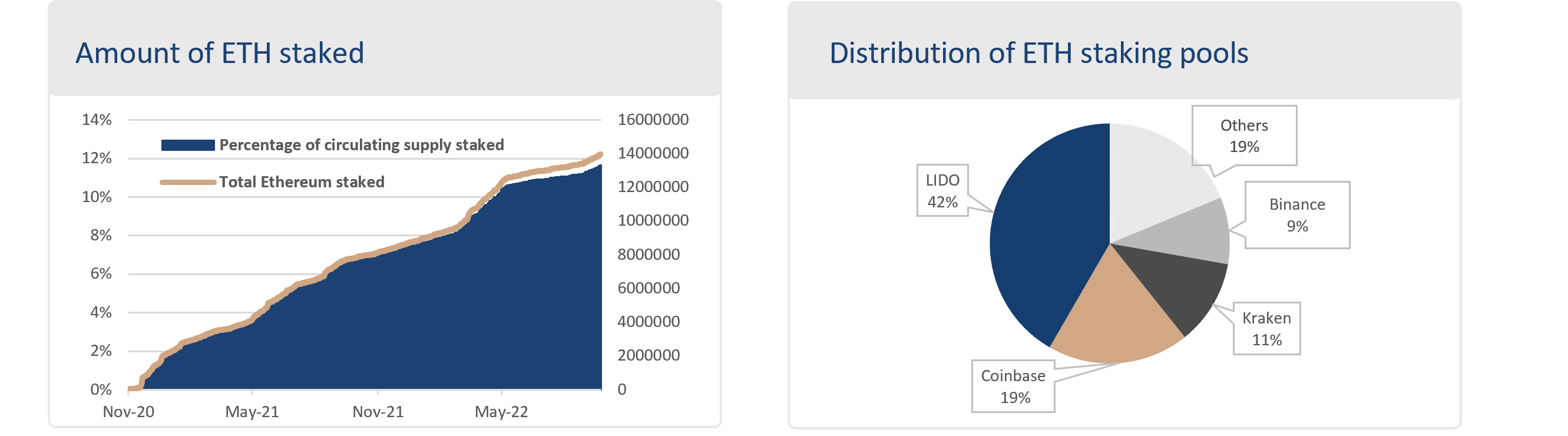

Ethereum staking & distribution

The amount of total ETH staked has been steadily increasing and has reached almost 12% of circulating supply. The largest staking pools are managed by the exchanges Coinbase, Kraken, and Binance, and the decentralised staking pool Lido, which could pose a centralisation risk.

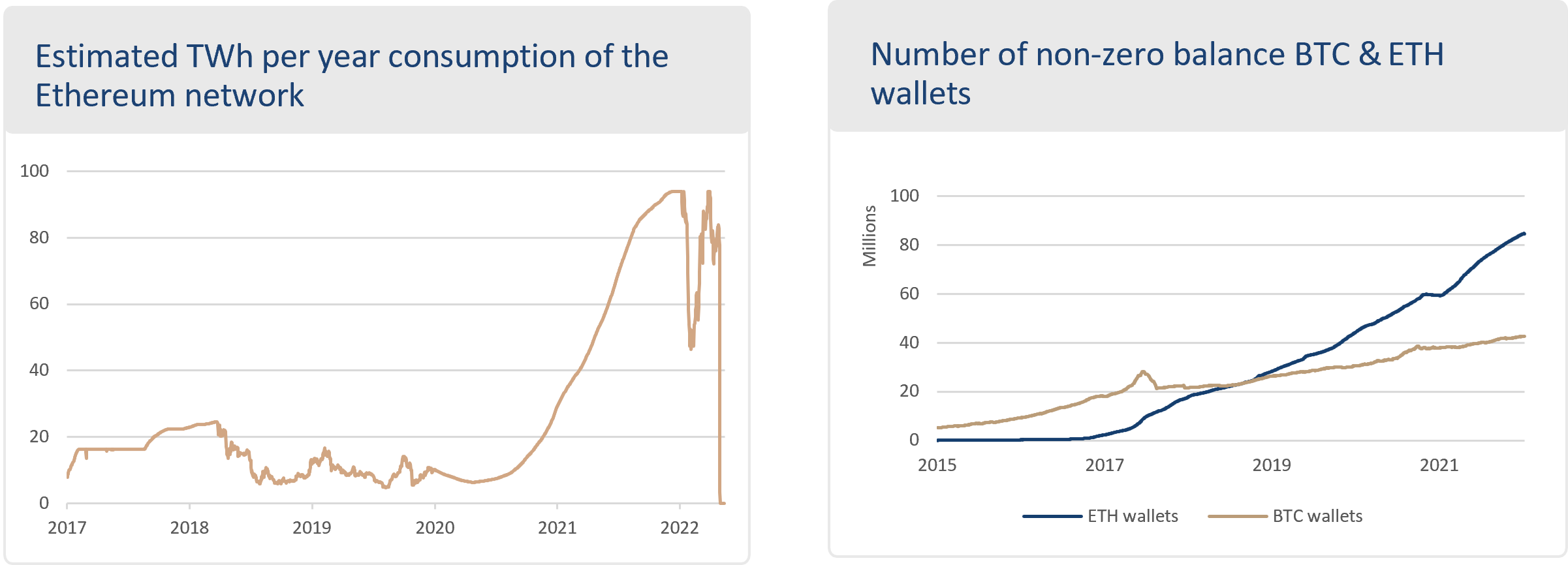

Ethereum power consumption & adoption

Ethereum power consumption has dropped over 99% since the merge. Adoption continues as can be seen by the ever-increasing number of non-zero balance wallets on both BTC and ETH networks.

2. Spotlight: Ethereum Merge

By Lukas Jelk, Sales & Business Development

The merge has marked the end of the proof-of-work consensus mechanism and the start of a new era for Ethereum. The transition to proof-of-stake was anticipated for years and finally successfully achieved on September 15th, 2022. The event “merged” the existing Ethereum PoW Mainnet and the PoS Chain, without any downtime. The network continued with the new PoS consensus mechanism and the same state.

Energy efficiency

The energy consumption of the network dropped by 99.95%. This was the main goal of the upgrade. Ethereum can now distance itself from power-hungry mining.

Rewards

The investment considerations for the ETH token changed since staking was implemented in 2020 and ETH became a reward-bearing asset. ETH owners can participate directly as a validator or delegate their ETH to a node operator and earn new ETH in the process. Rewards post-merge are forecasted between 8-12% p.a. However, these rewards may stay volatile depending on the amount of ETH staked and varying transaction fees. The unstaking of ETH remains deactivated for an unknown period. Also, if one is not staking, the ETH holdings get diluted, so investors have a strong incentive to stake.

Issuance and deflation

The annual issuance rate of new ETH from block rewards pre-merge was around 4.3%. Post-merge this rate was reduced by about 90% and is expected to be around 0.49% p.a. for the time being. Since a previous upgrade implemented the permanent removal of a part of the transaction fees from the supply, this could make Ethereum deflationary at times. Supply is expected to be flat or slightly deflationary over the next six months. The supply shock and less sell pressure due to absent miners might increase the assets value, if we see rising demand.

Concerns

With proof-of-stake, the Ethereum token became a vital part of the network’s security. A danger for PoS systems consequently stems from staking centralisation risks. Many ETH holders already rely on the same third parties for staking, which then have a substantial influence on the adherence to government regulations and censorship demands. In regard to security, PoS is less battle-tested than the older PoW consensus mechanism.

Outlook

Ethereum has a solid new foundation. The network is now “green” and more attractive to investors. The merge made Ethereum the largest environmentally-friendly blockchain network by market capitalisation and number of users. But crucial issues for mass adoption, such as lowering transaction fees and improving scalability, are still not resolved. More work lays ahead for the developers. Next year, scalability will be their target with the next upgrade called “The Surge”.

Terminology of the Month

Proof-of-Work (PoW): A crypto consensus mechanism, where the network is secured by miners racing to be the first to add a block to the blockchain, which requires processing power.

Proof-of-Stake (PoS): PoS is a consensus mechanism, which replaces the miners with validators, who contribute their own crypto assets as a “stake” in exchange for a reward. There is no race to be the first to add a block; instead validators are selected randomly to add the next block.

3. Trading Desk View

By Matteo Bottacini, Trader

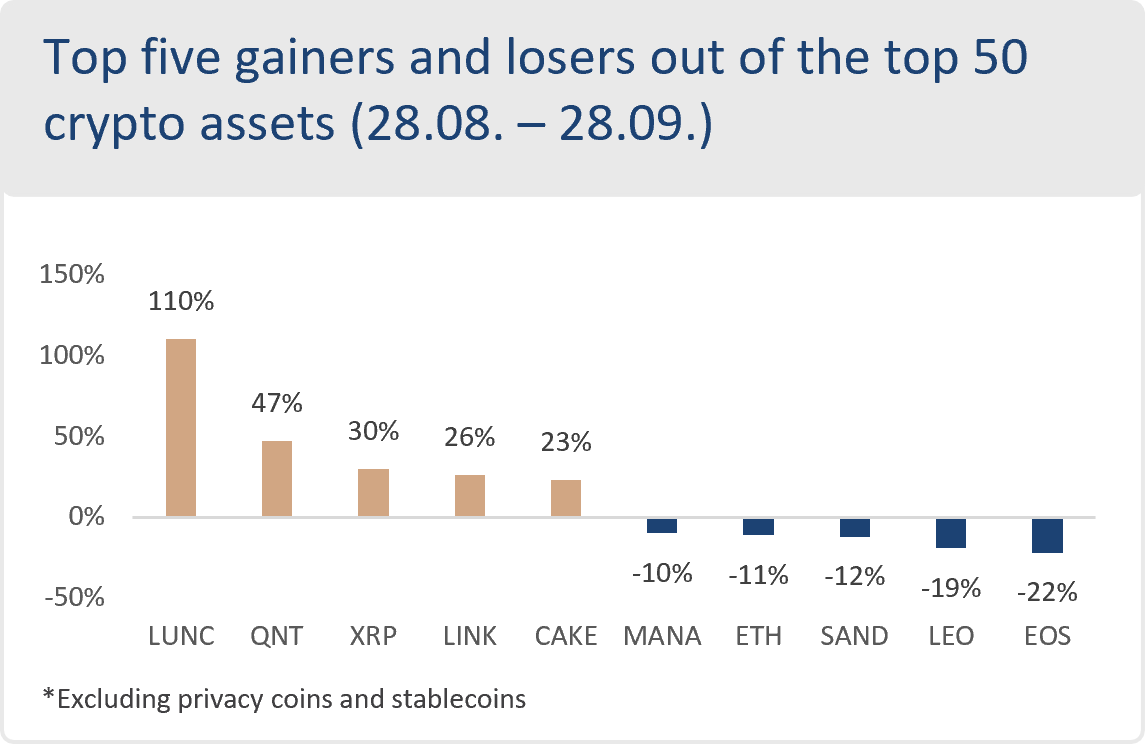

In the chart below you can see the 10 of the top 50 crypto assets ranked by market cap that have gained and the lost the most over the past month.

LUNC, the “old” LUNA coin, has emerged as the newest meme coin. Indeed, the tokenomics are broken (i.e., infinite circulating supply) and none of the core developers is supporting the project. But even a fish out of water bounces a couple of times.

XRP has been on a stellar run of late, rallying off hopes for a resolution in Ripple’s ongoing lawsuit with the SEC. The SEC and Ripple Labs filed for a “summary judgment” – a legal process where a court decides based on the facts that have been provided without ordering a trial. The recent XRP price action is another example of the kind of event-driven trading that is moving this market. XRP/BTC and XRP/ETH are at one-year highs. Looking at YTD returns, SAND and MANA, as part of the NFT and gaming industry, are heavily underperforming the market.

The Metaverse hype has somewhat vanished as the final and easy-to-use products seem far from finished (or, far from ready for mass adoption).

In periods of market turmoil, correlations among assets tend to increase and diversifications benefits disappear.

While the correlation between digital assets and the tech equities increased during the whole year, volatility decreased in the crypto space.

At present, bitcoin is trading at around 60% realised volatility for 30-days windows vs. 80% last year. The derivatives space evolved a great deal in terms of instruments and liquidity; systematic funds selling volatility and profiting from the big time-decay and the implied leverage in the crypto space are helping the market to achieve a more stable growth over time that will capture the attention of more traditional institutional clients.

Nevertheless, oracles and exchange tokens have one of the best business cases and are outperforming the market with a lower volatility even considering the smaller market cap.

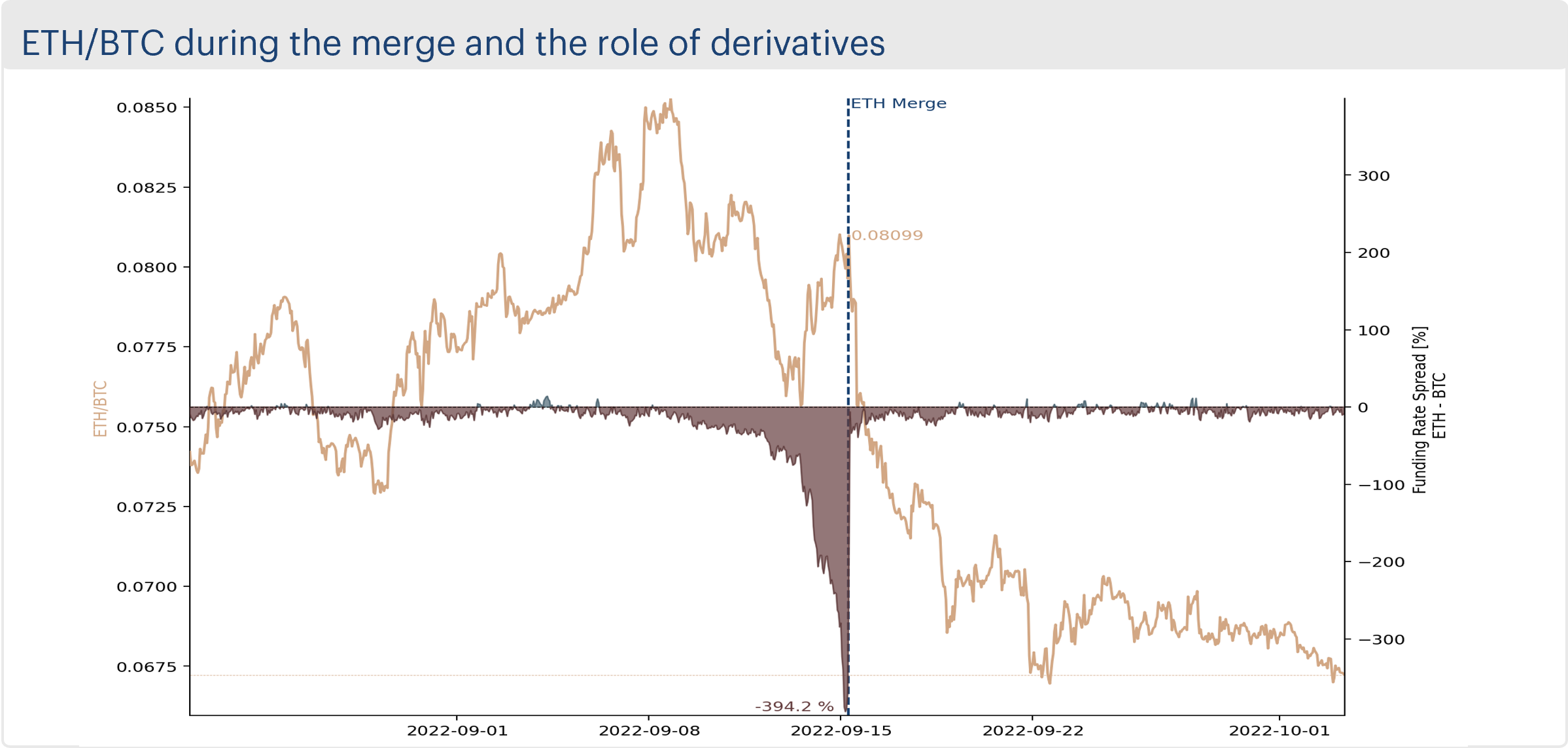

4. Topical Deep Dive: ETH/BTC

By Matteo Bottacini, Trader

Despite the successful ETH merge, the positioning of traders has been one-way since then. Since September 15th, ETH has underperformed BTC by 16.76%. This rally to the downside should not only be attributed to the adverse macro conditions. The merge is and has been an unequivocally bullish and risky event for Ethereum. If the merge had failed, it would have been catastrophic for the price of ETH and the crypto ecosystem in general.

Normally, a headline like “the merge” would have driven the market completely risk-on. However, risk was already on. On August 23rd, ETH/BTC was trading at 0.075 and topped 0.0856 (+14%) on September 7th. At the merge snapshot, ETH/BTC was trading at 0.08099 (+7.9%). At the time of writing, it is trading at 0.06724 (-10.34%).

The crypto space is getting crowded as more and more professional traders join the space, increasing the overall efficiency. Indeed, delta one traders were trying to get the most out of this event and bet on the ETH Proof-of-Work coin airdrop, in the case that there was a hard fork of the Ethereum blockchain.

Derivatives traders entered long positions on spot ETH and hedged the market exposure via futures. In normal market conditions, the basis spread, and the funding spread between ETH and BTC tends to zero. While a positive (negative) spread is typically a signal of bullish (bearish) market.

As the possibility of having an ETH PoW token materialised, the funding spread between the two pairs became wider and wider, and reached -394.2% annualised in the hour prior to the merge. Hedging one ETH via a Perpetual Future on FTX for the 24h prior the merge cost $12.18 (or 0.7585% ETH). In the four hours following the creation of the ETH PoW market on FTX, the coin was trading at an average of $22.98, equalling a profit of 88.73% excluding fees. FTX was one of the first exchanges to both credit the airdrop and to support trading of ETH PoW. All the market participants who had their Ethereum outside of FTX did not receive the token at that time, nor had the possibility to sell it on margin and cover the position later. Indeed, since the airdrop, the ETH PoW flow has been skewed to the sell side and it is now trading at $10.376, which is slightly below the “strike” price. This shows how the market is becoming more efficient and arbitrage free: any alpha out of these events is a risk-premia instead of an arbitrage profit.

As the market becomes more efficient, we expect that basis and funding spread will find a new equilibrium that will be reflected in the ETH PoS staking rewards, thus a 4-7% spread is realistic. At the time of writing, the spread between the funding rates is 5.36%, while the spread between the three-months basis is 3.59%.

Editorial Board

- Patrick Heusser, CEO Crypto Finance (Brokerage) AG

- Lewin Boehnke, Head of Research at Crypto Finance AG

- Stefan Schwitter, Head Asset Management at Crypto Finance (Asset Management) AG

Do you have questions or would like to subscribe to our reports? Please send an email to: assetmanagement@cryptofinance.ch. For more information also visit our website: www.cryptofinance.ch

All information in this document is provided for general information purposes only and with no warranty or liability for accuracy, completeness, or fitness for a particular purpose. No information provided in this document constitutes or is intended as investment advice. This document is not, and is not intended as, an offer, recommendation, or solicitation to invest in financial instruments including crypto assets. Crypto Finance is a financial group supervised by the Swiss Financial Market Supervisory Authority FINMA on a consolidated basis with Crypto Finance (Brokerage) AG as a securities firm and Crypto Finance (Asset Management) AG as an asset manager for collective investments with the corresponding FINMA licenses . This document and its content including any brand names, logos, designs, and trademarks, and all related rights, are the property of the Crypto Finance Group and Deutsche Börse Group. They may not be reproduced or reused without their prior consent.